How A Mortgage Calculator Can Save You Bundles Of Time

A mortgage calculator is perhaps the most valuable tool |

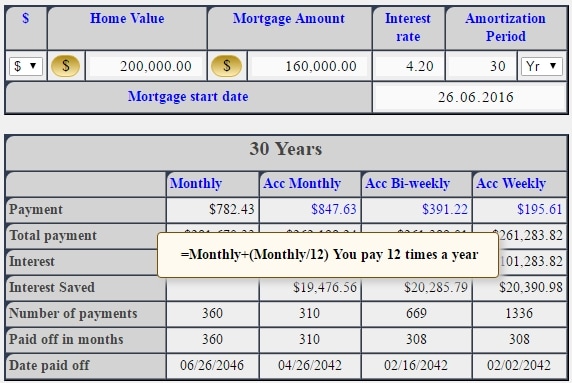

A mortgage calculator is perhaps the most valuable tool for anyone shopping for a new home. The reason is because a mortgage calculator can provide a variety of different figures, including monthly payments, affordability and interest costs. A mortgage calculator allows an individual to input his/her monthly income, monthly debt payments and returns an estimated amount on how much he/she can borrow for a mortgage loan. This number is only an estimate and cannot be used as a guarantee, but it certainly gives a prospective homeowner the knowledge to move forward with plans for home ownership.

|

The benefits to using a mortgage calculator are many |

|

Without a mortgage calculator, many first time homebuyers may go into the process without the proper knowledge |

Without a mortgage calculator, many first time homebuyers may go into the process without the proper knowledge or how much they can actually afford. You can find a mortgage calculator at mortgagecalculatorwithpmi.com. In today’s market, an individual’s debt must not exceed 50% of their total monthly income if they wish to get the best interest rates. If their debt to income ratio is higher than 50%, the borrower may be labeled as high risk and suffer higher interest rates or, in some cases, may be denied a loan altogether. An example would be an individual who earns $4,000.00 per month and wishes to purchase a home with monthly payments of $3,000.00. Because this number greatly exceeds 50% of the borrower’s take-home pay, he/she may be forced to find a home that is more affordable. The 50% debt to income ratio includes mortgage, auto and credit card payments.

|